Understanding how to calculate rental yield on a property is a fundamental skill for any real estate investor. Rental yield provides a clear percentage that represents the return on investment you can expect from a rental property based on its income and costs. Whether you are evaluating a single-family home, a multi-unit apartment building, or a commercial space, knowing the exact yield helps you compare different properties and make informed financial decisions. By analyzing both the gross and net rental yields, investors can assess the viability of a property, anticipate cash flow, and determine if the investment aligns with their long-term financial goals. This guide will walk you through the essential formulas, the difference between gross and net yield, and the various expenses you must account for to ensure your calculations are accurate and reliable. Mastering these concepts is the first step toward building a profitable real estate portfolio.

What is Rental Yield?

Rental yield is a financial metric used by real estate investors to measure the annual income generated by a property as a percentage of its total value or purchase price. It serves as a benchmark to evaluate the profitability of an investment property before factoring in capital appreciation. A higher rental yield generally indicates a more lucrative investment, although it is often accompanied by higher risks or maintenance requirements. Investors use this metric to quickly compare multiple properties in different markets and decide where to allocate their capital for the best possible returns. It is important to remember that yield is a snapshot in time; as property values and rental rates fluctuate, the yield will also change, requiring investors to monitor their assets continuously.

Gross Rental Yield vs. Net Rental Yield

When learning how to calculate rental yield on a property, it is crucial to distinguish between gross rental yield and net rental yield. Gross rental yield is the simplest calculation, as it only considers the total annual rent collected relative to the property value. It does not account for any operating expenses, making it a useful tool for a quick, high-level overview when scanning numerous listings. Net rental yield, on the other hand, provides a much more accurate picture of your actual return. It subtracts all operating expenses—such as property taxes, insurance, maintenance, and property management fees—from the annual rental income before dividing by the property value. Relying solely on gross yield can be misleading, as properties with high gross yields often have hidden costs that severely diminish the net return.

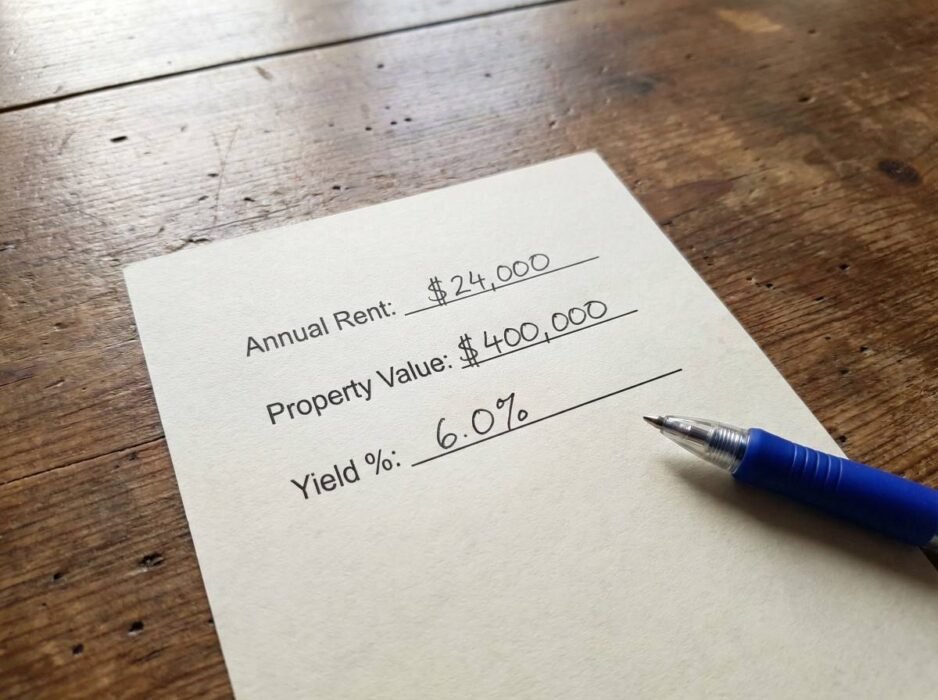

How to Calculate Gross Rental Yield

Calculating the gross rental yield is a straightforward process that requires only two figures: the total annual rental income and the property value or purchase price. The formula is simple: divide the annual rental income by the property value, and then multiply the result by 100 to get a percentage.

For example, if you purchase a property for $300,000 and rent it out for $2,000 per month, your annual rental income is $24,000. Dividing $24,000 by $300,000 gives you 0.08. Multiplying by 100 results in a gross rental yield of 8%. While this number is helpful for initial comparisons, it does not reflect the true profitability of the property since it ignores the costs associated with owning and operating the real estate. Investors typically use gross yield to filter out properties that do not meet their minimum return thresholds before conducting a deeper financial analysis.

How to Calculate Net Rental Yield

To calculate the net rental yield, you must first determine your net operating income (NOI). This involves adding up all your annual operating expenses and subtracting them from your gross annual rental income. Common expenses include property taxes, landlord insurance, homeowners association (HOA) fees, routine maintenance, vacancy costs, and property management fees. Note that mortgage payments are typically excluded from this calculation, as yield measures the property’s performance rather than the investor’s financing structure.

Once you have the net operating income, divide it by the total property value or purchase price, and multiply by 100. For instance, if the same $300,000 property generates $24,000 in gross rent but incurs $8,000 in annual expenses, the net operating income is $16,000. Dividing $16,000 by $300,000 equals approximately 0.0533, which translates to a net rental yield of 5.33%. This figure is much more reliable for determining whether the property will generate positive cash flow and meet your investment criteria.

Comparing Gross and Net Rental Yield

Understanding the difference between these two metrics is vital for accurate financial planning. The table below illustrates a comparison between gross and net rental yield calculations for a hypothetical investment property, highlighting how expenses impact the final percentage.

| Metric | Gross Rental Yield | Net Rental Yield |

|---|---|---|

| Property Value | $300,000 | $300,000 |

| Monthly Rent | $2,000 | $2,000 |

| Annual Rental Income | $24,000 | $24,000 |

| Annual Operating Expenses | $0 (Not factored) | $8,000 |

| Net Operating Income | $24,000 | $16,000 |

| Calculated Yield | 8.00% | 5.33% |

As demonstrated in the table, relying solely on gross yield can lead to an overestimation of a property’s profitability. Always calculate the net yield to ensure you have sufficient cash flow to cover unexpected repairs, ongoing maintenance, and periods of vacancy.

What is a Good Rental Yield?

A common question among investors is what constitutes a “good” rental yield. The answer largely depends on the local real estate market, the property type, and the investor’s individual strategy. In many US markets, a net rental yield between 5% and 8% is considered healthy for residential properties. Properties in high-demand urban areas may offer lower yields due to higher purchase prices, but they often provide stronger capital appreciation over time. Conversely, properties in rural or economically depressed areas might show double-digit yields on paper, but they carry higher risks of prolonged vacancies, extensive maintenance issues, and stagnant property values. Investors must balance the desire for high yield with the reality of market risks and property conditions.

Frequently Asked Questions

Does rental yield include mortgage payments?

No, rental yield calculations typically exclude mortgage payments and interest. Yield is designed to measure the income-generating performance of the property itself, independent of how the purchase was financed. If you want to measure your return based on the cash you actually invested, including your down payment and financing costs, you should calculate the cash-on-cash return instead.

How do vacancy rates affect rental yield?

Vacancy rates have a direct and significant impact on your net rental yield. When a property sits empty, it generates zero income while operating expenses like taxes, insurance, and utilities continue to accrue. It is standard practice to factor in a vacancy rate—often between 5% and 10% of the gross income, depending on the local market—when estimating your annual rental income for yield calculations.

Should I focus more on rental yield or capital growth?

The choice between rental yield and capital growth depends entirely on your investment goals. If you need immediate, consistent cash flow to supplement your income or cover expenses, prioritizing high rental yield is advisable. If you are investing for long-term wealth accumulation and can comfortably cover short-term expenses, focusing on properties with strong capital appreciation potential may be more beneficial.

Are property management fees included in net yield calculations?

Yes, property management fees are a standard operating expense and must be subtracted from your gross rental income when calculating net rental yield. These fees typically range from 8% to 12% of the monthly rent and significantly reduce your net operating income, making them a crucial factor in your profitability analysis and overall investment strategy.

How often should I recalculate the rental yield on my property?

You should recalculate your rental yield annually or whenever there is a significant change in your rental income or operating expenses. Property taxes, insurance premiums, and market rent rates fluctuate over time. Regular recalculations ensure that your investment continues to perform according to your financial expectations and helps you decide when it might be time to adjust rent, refinance, or sell the property.

Conclusion

Mastering how to calculate rental yield on a property empowers you to make objective, data-driven real estate investment decisions. By understanding the distinction between gross and net yield, accurately estimating your operating expenses, and factoring in variables like vacancy rates, you can accurately project your cash flow and assess the true profitability of an asset. Whether you are a novice buyer evaluating your first single-family home or an experienced landlord managing a large portfolio, consistently applying these formulas will help you build a resilient and profitable real estate business. Always prioritize net yield over gross yield to ensure your investments are truly working for you.