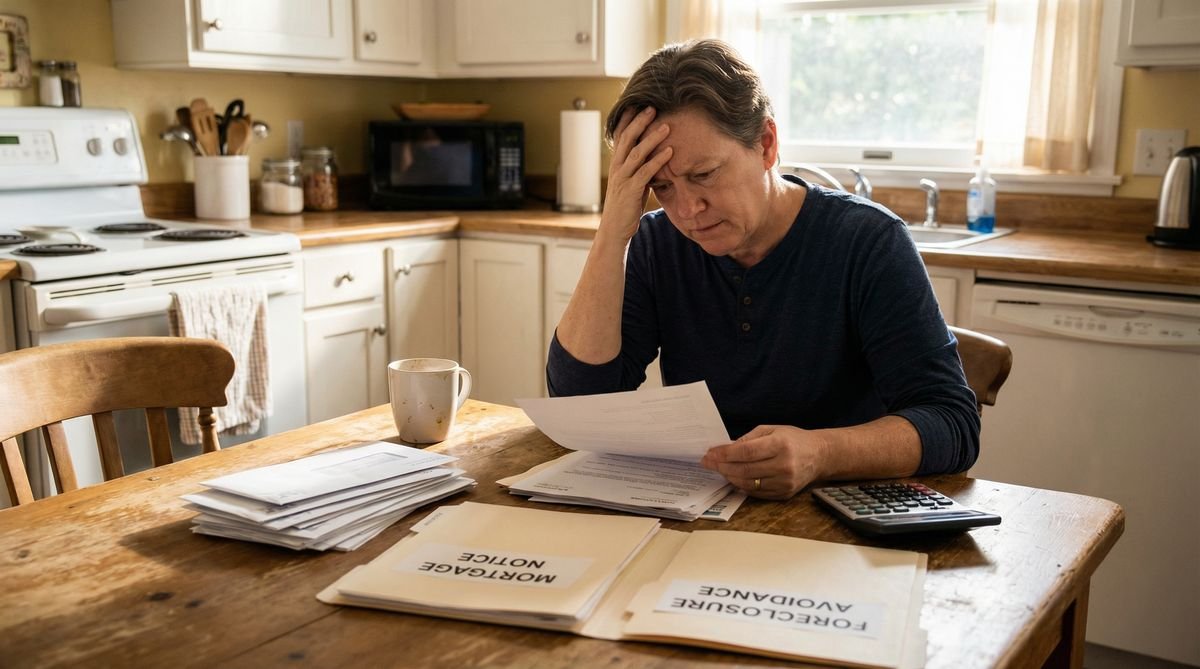

When facing financial hardship, homeowners might explore various options to avoid foreclosure. One such option, often misunderstood, is a short sale in real estate, Freshstart Property Management experts notes that this process allows a homeowner to sell their property for less than the outstanding mortgage balance, with the lender agreeing to accept the reduced payoff.

Understanding what a short sale entails is crucial for anyone involved in the real estate market, whether as a distressed homeowner, a potential buyer, or an agent. It’s a complex transaction with specific criteria and potential pitfalls, but it can offer a viable path forward for all parties if managed correctly.

Defining a Real Estate Short Sale

At its core, a short sale occurs when a property’s market value has fallen below the amount the homeowner owes on their mortgage. Instead of going through a lengthy and damaging foreclosure, the lender agrees to let the homeowner sell the property for its current market value, even if that amount is “short” of what is owed. The lender then typically forgives the remaining balance or negotiates a repayment plan.

This isn’t a simple transaction; it requires the lender’s explicit approval and often involves extensive negotiation. The primary goal for the homeowner is to mitigate the negative impact on their credit and avoid foreclosure, while the lender aims to recover as much of their investment as possible without the added costs and time associated with a foreclosure.

The Short Sale Process: A Step-by-Step Overview

Engaging in a short sale is a multi-stage process that demands patience and careful execution. Here’s a general outline of how it typically unfolds:

- Financial Hardship Documentation: The homeowner must prove genuine financial hardship to their lender. This usually involves submitting detailed financial statements, tax returns, and a hardship letter explaining their inability to make mortgage payments.

- Property Valuation: The lender will order an appraisal or a Broker Price Opinion (BPO) to determine the property’s current market value. This helps them assess the potential loss.

- Listing the Property: The homeowner lists the property for sale, often with an agent experienced in short sales. The listing price is typically based on the property’s market value, not the outstanding mortgage balance.

- Receiving an Offer: Once a buyer submits an offer, it is presented to the lender for approval. This offer must be reasonable and reflect current market conditions.

- Lender Negotiation and Approval: This is often the longest and most challenging phase. The lender reviews the offer, the homeowner’s financial documents, and the property valuation. They may counter-offer or request additional information.

- Closing the Sale: If the lender approves the offer, the sale proceeds like a traditional real estate transaction, with the lender accepting the agreed-upon amount as full or partial satisfaction of the debt.

Who Benefits from a Short Sale?

While seemingly complex, a short sale can offer advantages to all parties involved compared to a foreclosure.

For the Homeowner

- Avoids Foreclosure: A short sale is generally less damaging to a homeowner’s credit than a foreclosure.

- Debt Relief: Lenders may forgive the remaining mortgage balance, though this can have tax implications.

- Control: Homeowners have more control over the sale process than in a foreclosure.

For the Lender

- Minimizes Losses: Lenders often recover more money through a short sale than through a foreclosure, which incurs significant legal and maintenance costs.

- Faster Resolution: Short sales can be quicker than foreclosures, reducing carrying costs for the lender.

For the Buyer

- Potential for a Good Deal: Buyers might acquire a property at a price below market value, though this isn’t guaranteed.

- Clear Title: Unlike some foreclosure sales, short sales typically come with a clear title, as the lender is involved in the transaction.

Short Sale vs. Foreclosure: A Critical Comparison

Understanding the distinctions between a short sale and a foreclosure is vital for homeowners facing financial distress. While both involve a homeowner losing their property, the implications for their financial future and credit score differ significantly.

| Feature | Short Sale | Foreclosure |

|---|---|---|

| Credit Impact | Less severe; typically a 100-200 point drop, potentially recoverable in 2-3 years. | Severe; typically a 200-300+ point drop, remaining on credit report for 7 years. |

| Control over Sale | Homeowner has some control over listing and showing the property. | Lender takes full control; homeowner has no say in the sale process. |

| Deficiency Judgment | Often waived by lender, but can be negotiated. | Lender can pursue a deficiency judgment in many states. |

| Future Mortgage Eligibility | Possible to qualify for a new mortgage in 2-4 years. | Typically 3-7 years before qualifying for a new mortgage. |

| Privacy | More private; sale is a standard real estate transaction. | Public record; can be emotionally distressing. |

Common Myths and Misconceptions About Short Sales

The complexity of short sales often leads to several misunderstandings. Let’s debunk a few common myths:

Myth 1: Short Sales are Always a Steal for Buyers

While buyers can sometimes get a good deal, it’s not guaranteed. Lenders want to minimize their losses, so they won’t approve offers significantly below market value. The process can also be lengthy, testing a buyer’s patience.

Myth 2: Homeowners Get to Keep the Proceeds

Absolutely not. All proceeds from a short sale go directly to the lender to pay down the mortgage. The homeowner receives no money from the sale.

Myth 3: Short Sales are Quick Transactions

Quite the opposite. The need for lender approval and negotiation can extend the closing process for several months, sometimes even a year. This requires significant patience from both buyers and sellers.

Key Considerations for a Successful Short Sale

For homeowners considering a short sale, several factors are paramount:

- Seek Expert Advice: Engage a real estate agent experienced in short sales and consult with a real estate attorney and tax advisor.

- Honest Communication: Be transparent with your lender about your financial situation.

- Patience: The process is often long and requires persistence.

- Deficiency Judgment: Understand if your state allows deficiency judgments and negotiate with your lender to waive it if possible.

Conclusion

A short sale in real estate offers a critical alternative for homeowners facing financial distress, providing a path to avoid the more severe consequences of foreclosure. While it demands patience and careful navigation, understanding its intricacies can empower both sellers and buyers to make informed decisions.

By working with experienced professionals and thoroughly understanding the process, a short sale can be a strategic move that benefits all parties, allowing homeowners to move forward and buyers to potentially find a valuable property. It’s a testament to the dynamic nature of the real estate market and the options available even in challenging circumstances.