According to MHN Property Management team, purchasing a home is one of the most significant financial decisions many Americans make, and while the down payment and mortgage principal often dominate discussions, another crucial financial aspect frequently surprises buyers: closing costs. These are a collection of fees and expenses paid at the closing of a real estate transaction, beyond the purchase price of the property itself. They cover a range of services from loan origination to title transfer, ensuring the transaction is legally sound and properly recorded. Understanding these costs upfront is essential for accurate budgeting and avoiding last-minute financial stress. Typically, closing costs can range from 2% to 5% of the loan amount, but this can vary significantly based on location, loan type, and specific service providers. Being prepared for these additional expenses is key to a smooth and successful home buying journey.

What Are Closing Costs?

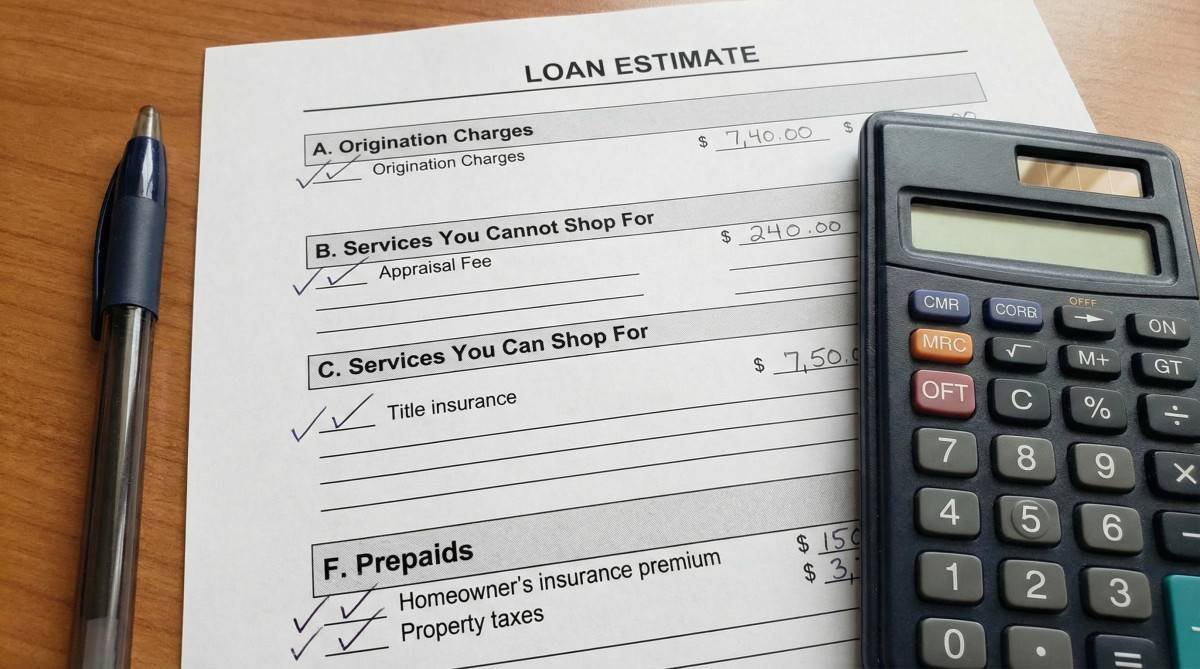

Closing costs encompass a broad spectrum of fees charged by various parties involved in the home buying process. These can include lenders, title companies, attorneys, and local government entities. They are not part of your down payment but are necessary to finalize the mortgage and transfer ownership of the property. The specific costs you’ll encounter depend on several factors, including your loan type (e.g., FHA, VA, conventional), the state and county where you’re buying, and the service providers you choose. Some costs are one-time fees, while others might be prepaid expenses that cover future obligations like property taxes or homeowner’s insurance premiums.

Common Types of Closing Costs

Closing costs can be categorized into several main groups. Understanding these categories helps in identifying where your money is going:

- Lender Fees: These are charged by your mortgage lender for processing your loan. Examples include loan origination fees (typically 0.5% to 1% of the loan amount), application fees, underwriting fees, and discount points (paid to lower your interest rate).

- Third-Party Service Fees: These cover services provided by external professionals. This category includes appraisal fees (typically $300-$600), credit report fees ($30-$50), and flood certification fees.

- Title and Escrow Fees: Title insurance protects both the lender and the homeowner from disputes over property ownership. Title search fees ($200-$400) ensure a clear title, while title insurance premiums can be substantial, often hundreds to thousands of dollars depending on the home’s value. Escrow fees are paid to the escrow company or attorney for managing the closing process.

- Government Recording Fees and Taxes: These are fees paid to local government to record the new deed and mortgage. Transfer taxes, if applicable in your state or county, can be a significant expense, sometimes reaching 1% to 2% of the property’s value.

- Prepaid Expenses: These are not technically closing costs but are often paid at closing. They include property taxes for a certain period, homeowner’s insurance premiums for the first year, and potentially mortgage interest for the remaining days of the month you close.

How Much Do Closing Costs Typically Add?

As a general rule of thumb, closing costs typically range from 2% to 5% of the loan amount. However, this is a broad estimate, and the actual percentage can fluctuate. For instance, on a $300,000 home with a $240,000 loan, closing costs could range from $4,800 to $12,000. It’s crucial to remember that this percentage is usually based on the loan amount, not the home’s purchase price, although some fees like transfer taxes might be based on the purchase price. The average closing costs in the U.S. can vary significantly by state, with some states having higher transfer taxes or unique local fees. For example, states like New York and Pennsylvania often have higher closing costs due to higher transfer taxes and other local regulations, while states like Missouri and Indiana tend to have lower costs.